In this article

On September 18, the Fed announced it would drop interest rates by 50 basis points. Even though there’s a flurry of articles hot off the press about the potential impacts of this decision, most people don’t understand the nuts and bolts of what’s going on. Who can blame them? It’s easy to get buried in a sea of complicated jargon and double-speak. But that’s the exact opposite of how we view it.

So, in this article, we’ll do a deep dive into what that means for mortgage rates in Georgia and how that impacts you.

Although the first part of this may feel like one of those boring classes you were forced to take senior year, we promise it will be worth it. It’s not as complicated as you might think. It all comes down to the fundamental law of supply and demand, and if you understand how supply and demand works, interest rates are simple.

Basic Supply and Demand

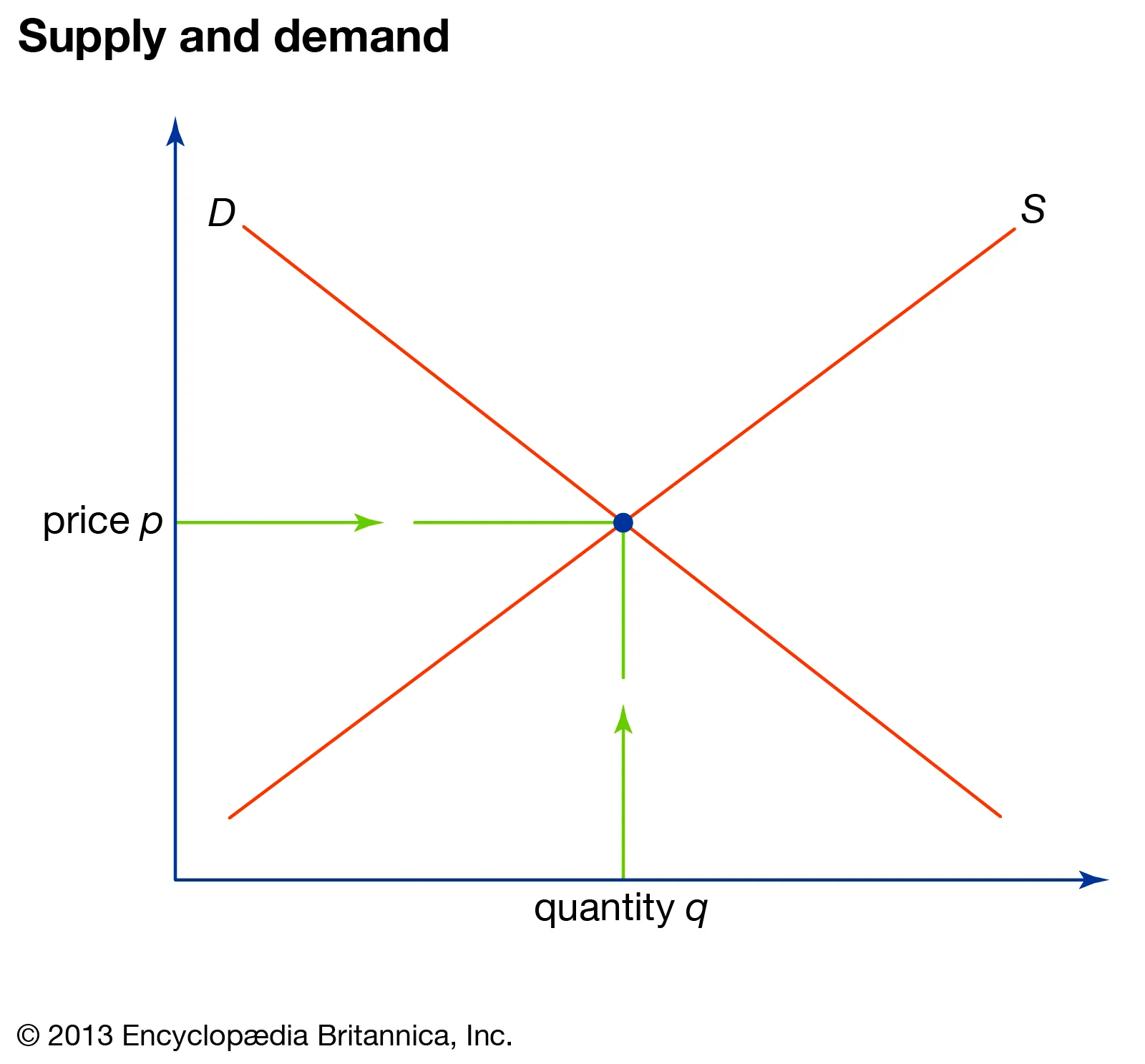

Let’s start by taking a look at a simple supply and demand graph:

As you can see, the price appears on the vertical axis. Quantity is our y-axis (or independent axis). Adjustments made to price affect quantity on the x-axis (or dependent axis). Quantity is dependent on price.

Inside the graph, two red lines tell us about supply and demand. The supply curve rises from left to right. All this means is that people make more stuff as the value of that stuff increases. More people will want to sell a product or service as its price increases.

The demand curve descends from left to right. As the price of a good or service decreases, the quantity people want to buy increases.

The point in the middle is called the equilibrium. In an efficient market, price and quantity trend towards this equilibrium point in the middle. It’s the natural balance point on the teeter-totter of the marketplace.

But how does this all apply to interest rates? It all starts to make sense when we realize that the interest rate is nothing more than the price of borrowing money. But to fully explain it, we have to cover one more concept.

Interest Rates and Loanable Funds

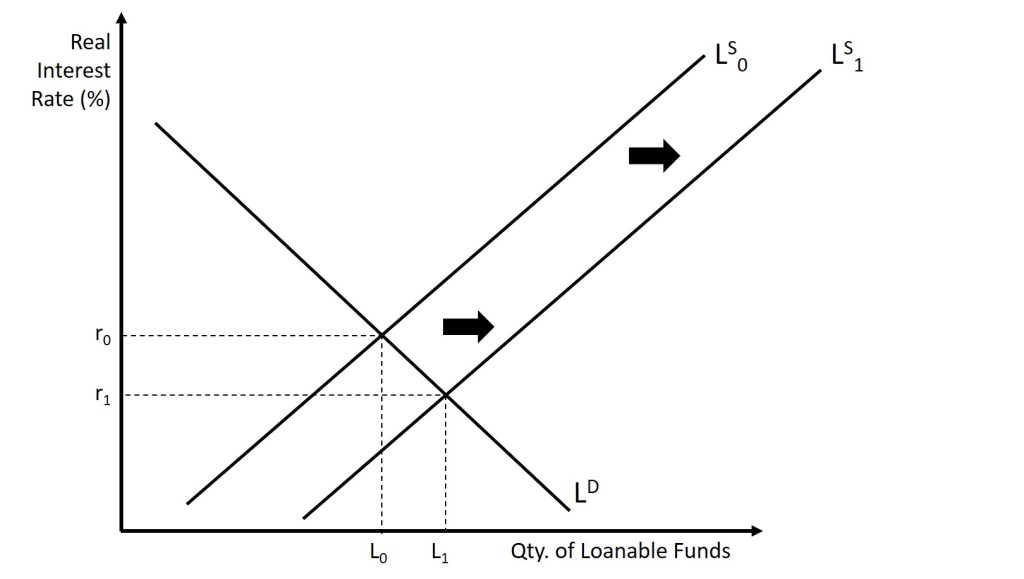

Look at this graph:

For simplicity, we replaced price with the interest rate, and the quantity denotes the amount of loanable funds. You probably also noticed we’ve added a second supply curve. This second supply curve is called a shift. It happens when the Fed lowers the interest rate – the equilibrium for money to borrow and invest (quantity) increases.

The Fed wants to create more investment because investment is a component of the national gross domestic product (GDP). GDP is basically how we measure national economies. It’s the sum of consumption, investment, government spending, and net exports.

Lower interest rates (cost of borrowing money) lead to more investment, which grows the economy. Lower rates also lead to more purchasing activity and consumption.

However, this may prompt the question of why the Fed ever increased interest rates to begin with. Why not set the rate in the basement at 1% and leave it there until the end of time?

Inflation.

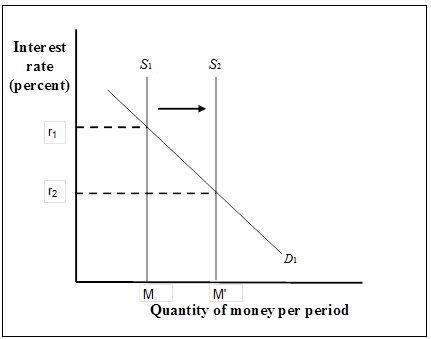

This leads us to discuss how the Fed achieves a lower interest rate. It’s not enough for the Fed to come out and say there’s a lower interest rate. They do it by buying bonds, which increases the money supply. Look at this graph:

As you can see, a decrease in the interest rate also means an increase in the overall money supply. And as the overall money supply increases, so does inflation. The mechanism by which this happens is the Fed dumping money into the economy by purchasing government and even AAA corporate bonds.

So what does all this mean? The reason the Fed raised interest rates to begin with was to shrink the money supply and curb high inflation rates. However, there’s significant pressure to lower it again because inflation is under control and the market is stagnant, especially the housing market.

Interest Rates, Mortgages, and The Housing Market

Lowering the interest rate has several implications, but we will focus on the mortgage market. Remember, the interest rate is the cost of borrowing money. And since the cost of borrowing money is coming down, more people will be jumping into the market.

This could mean that for first time home buyers, the benefit of the rate cut will be marginal.

As the rates come down, demand for houses will rise. One the smallest scale, this means shoppers will have to compete with other potential buyers when making an offer. On a larger scale, that increased demand will lead to increased prices.

Down payments will be slightly higher, and monthly payments will remain similar. The upside is that, with a lower interest rate, more of the monthly payment goes towards the principal resulting in a faster accrual of equity.

One the other hand, if you’ve had the down payment money for a while and were waiting for a lower rate, the environment is getting friendlier. But, you don’t have to be in a rush, as more rate cuts are probably in the pipeline.

The people who are going to benefit the most are refinancers. Those who bought houses during rate hikes are in a prime position to consider refinance options.

But even if you’re positioned to benefit from a refinance, you don’t have to be in a rush since there’s likely to be another 75 basis points in rate cuts by the end of 2024.

Ride the Wave Down

When rates are projected to continue falling slowly, homeowners with some amount of equity in their home (sometimes as little as six mortgage payments) can refinance their loan to a lower rate.

Refinancing a loan isn’t free, but if you refinance during a rate-cut period, you can roll the costs of your mortgage into the new principal, which will still lower your monthly payment.

Let The Moreira Team work for you!

Regardless of economic circumstances, getting the most for your money is always our top priority. Whether you’re a first time home buyer or refinancing your current mortgage, the Moreira Team works hard to get you the best deal on your mortgage or refinance.

We offer dozens of loan types and terms, so your mortgage and monthly payment work for you. We also have access to rates from 28 lending institutions, meaning you get the best possible terms as the market shifts. Contact us today to see what we can do for you.